Have you ever wondered how some crypto sites can offer ludicrous APRs? Here’s a short primer to dive in – and as this is a primer, some concepts/ background are edited for clarity.

Some of the most promising sites/ tech in DeCentralized Finance (DeFi) are DEXs. A DEX (decentralized exchange) facilitates trading round the clock, every day of the year, without requiring a username or password. You retain custody of your crypto on your own cold wallet hardware (say Ledger or Trezor). Once the transaction is recorded on the blockchain the ownership/ settling of the asset is done automatically – there is no T+2 settlement like in TradFI (Traditional Finance).

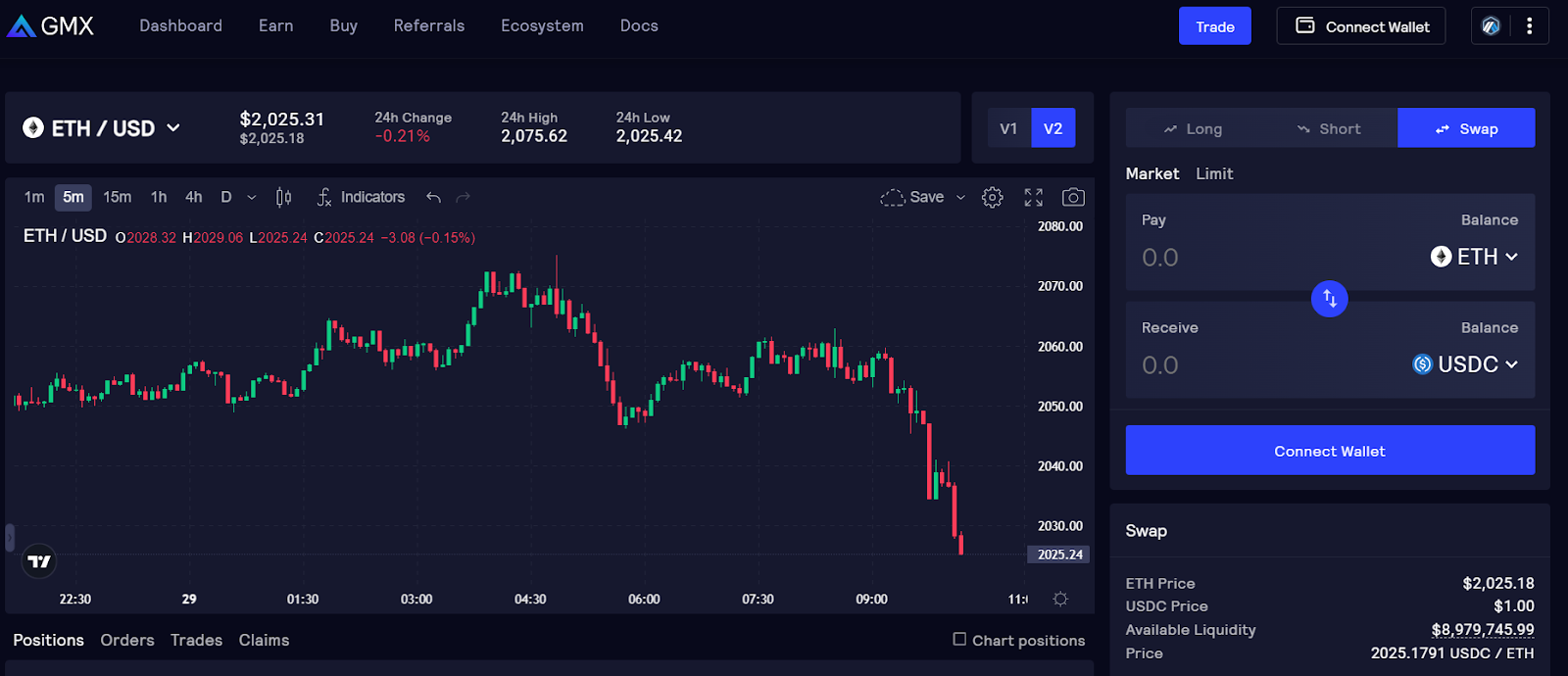

Let’s use GMX (on Arbitrum / Avalanche) as an example – if you want to swap say your ETH to USDC, you go to the Trade page and execute your trade just like you would on a centralized exchange:

Now, you may ask yourself – all these centralized exchanges (Coinbase, Binance, Nasdaq, NYSE, GS dark pools etc) – how do they make money? Well, they make their money on trading – pairing Bob who wants to buy ETH for $2000 from Alice, and charging a fee (price difference or transaction fee) for the service.

Imagine that all for example ETH owners, including Bob, could “Pool” their ETH (in a Liquidity Pool), allowing them to earn fees on ETH trades. Essentially the ETH is placed in a ‘vault’ or smart contract that pools your ETH with other DeFi users. Then you as a “Liquidity Provider / LP” earn a good chunk of the fee revenue that accrues to the pool – as a percentage of your ownership in the pool.

Throughout history a centralized/ third party has earned these fees. With DeFi you still custody the assets (you are the only one with the private keys). This is at the core of DeCentralized Finance – getting rid of the intermediaries, and allowing the actual owners of the assets to benefit.

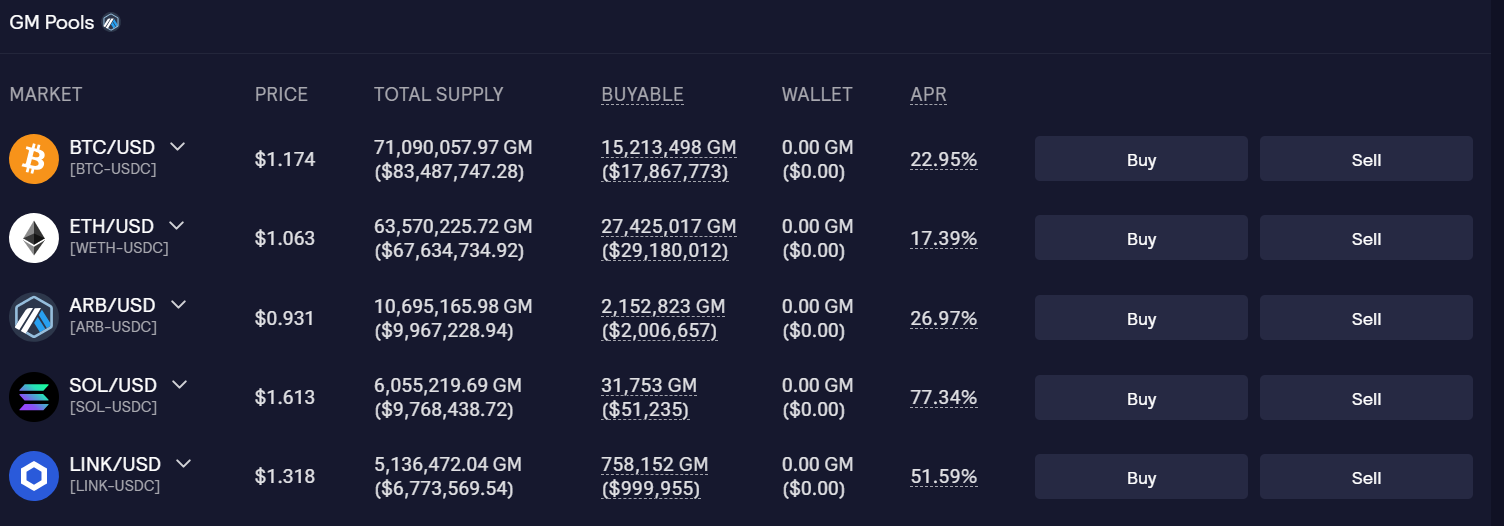

So what kind of rates can earn in these pools? On GMX V2 pools today:

And we’ve heard Ethereum transactions are expensive right? GMX runs on Arbitrum – an ETH Layer 2, and transactions are normally 10c-20c… (and will get cheaper..).

Remember these are new technologies, where some sites/ users have been hacked, you take on smart contract risk, risk of owning the crypto asset etc, but it’s not ‘Fake SBF / Terra Luna’ yield, it is native yield based on fee generation. Always do your due diligence on the sites you use – personally I prefer the larger DeFi sites with a higher TVL (total value locked), higher revenues, clear open-source code on Github for all key functionalities etc…

Finally – this is NOT financial advice, be careful out there 🙂

Taylor Swift isn’t just a music icon; she’s also on the front lines of changing how stars and fans connect. She’s created a passionate community, taken on big music companies, all while being aligned ethically with what’s called Web 3 – let’s dive in how…

Building a Fan Family

Taylor’s fans, the “Swifties,” aren’t just cheering from the sidelines; they’re part of the conversation. She talks to them straight through social media, not just to share music news but to get their take on things, too. Swift’s approach to engaging with her community directly, without going through traditional media or platforms that might act as intermediaries, also aligns with the Web 3 principle of decentralization. This creates a tight-knit fan club – whereas Web 3 technologies can provide the tools for online communities to decide how they want to govern themselves, how the community is built etc.

Cutting Out the Middleman

Taylor’s bold move to re-record her old songs is a game-changer. It’s her way of taking back control and getting closer to her fans without the music industry’s big players calling the shots. In 2019, Swift spoke out against the acquisition of her master recordings by Scooter Braun’s Ithaca Holdings as part of its deal with Big Machine Records. She emphasized the importance of artists owning their masters to control their work’s usage and financial benefits. It’s similar to what Web 3 wants to do—cutting out the unnecessary middleman and letting creators sell their art to their most hard-core fans. Imagine owning an NFT, that for example gives access to alternative versions of songs, or allows the owner to receive a share of the song’s royalties.

Music for Everyone

Swift’s ethical alignment with Web 3 is underscored by her advocacy for artist rights and fair compensation. Her public battles against inequitable streaming revenues and ownership rights echo the Web 3 emphasis on fair value distribution and transparency. For example in 2014, she removed her entire catalog from Spotify, protesting against its streaming royalties’ distribution model. In the Web 3 world, smart contracts on blockchain platforms could ensure artists receive their due share without the opacity that sometimes shrouds the financial flows of the music industry, or could allow the platforms themselves to be owned by the artists and fans.

Advocating for Fellow Artists

In 2015, Swift wrote an open letter to Apple Music, criticizing their policy not to pay artists during the service’s free three-month trial period. Apple reversed its policy following Swift’s letter, agreeing to pay artists even during the trial. This action reflected a Web 3-type advocacy for transparent and fair compensation models that benefit all stakeholders.

Avoiding scalpers

With tickets to concerts often costing $1000’s of dollars due to scalpers, blockchain-based systems can enforce identity verification and purchase limits at the point of sale. Smart contracts can be programmed to allow only verified users to purchase tickets and limit the number of tickets each user can buy. This reduces the likelihood that scalpers can buy large quantities of tickets for resale at inflated prices.

Challenges to Think About

The music industry is deeply entrenched in its ways, and a single artist, irrespective of their influence, can face significant hurdles in changing the system. Additionally, the Web 3 space is still in its infancy, and its principles, technologies are yet to be tested at scale, especially in creative industries.

Conclusion

Taylor Swift is not just writing anthems for generations but also rewriting the rulebook on how artists and communities interact in the digital age. She’s showing us a peek into a future where music and the internet can be a place where everyone wins, with artists in charge of their own music and fans getting front-row seats to the show.

As I’m getting frequent questions from my ‘non-crypto’ friends re: why I like crypto and ETH in particular, here is my take as it stands today (March 2022).

TLDR version

The coming POS upgrade will enable large institutions to invest as the Proof of Work / ESG complication is removed.

The supply of ETH will drop in June from 12,000 ETH per year to 1,200 ETH per year which will all go to the holders of ETH.

Staking rewards will rise from the current 5% pa to 10-15% pa

ETH is growing like a rocket, with usage up 10x just in 2021

In the aftermath of Canadian truckers and Russian sanctions, the importance of de-centralization will increase, working against ETH challengers like SOL, FTM, Terra etc.

Background

Ethereum is the first ‘programmable blockchain’ with the whitepaper written by Vitalik Buterin in 2014, and the blockchain was launched in 2015. The genesis block was mined, so Ethereum today is a Proof of Work (PoW) blockchain.

Ethereum use cases

Ethereum enables a vast array of ‘decentralized applications’ or ‘dapps’ to be launched on top of it. The dapps are essentially smart contracts (programs) that run on Ethereum, and fees denominated in Ether (the native Ethereum currency) are paid (currently to PoW miners) to record the transactions on the Ethereum blockchain.

Dapps cover a wide array of use cases:

Decentralized Finance / DeFi – where the dapps today provide almost all of the services you can find in traditional finance (trad fi) – such as lending, staking, trading, options, etc. Yields on crypto assets in DeFi can often be very lucrative, with ‘stablecoins’ (e.g USDC – that is US Dollars on a Ethereum) you can earn yields of 8% to 19% p.a. with no fluctuating crypto prices. What is the interest you are getting in your current bank account?

The most popular DeFi dapps include Uniswap, Sushiswap, MakerDao etc. Just to be crystal clear here these are all autonomous programs that “live” on the Ethereum chain, and carry out all those functions with no human intervention. This is why banks are worried about ‘disintermediation’ from DeFi- meaning that banks would be put out of business.

NFTs – or NonFungible Tokens enable creators or communities to prove digital ownership of an asset, membership or status. The use cases range from:

Music – e.g. music artists being able to offer their fans different levels of interaction – where die-hard fans could buy access to a VIP lounge after a concert, or access to a discord channel with early releases of the artists more experimental music. This enables a ‘tiered pricing model’ which is much more favorable for the artists and fans.

Sports – sites like NBA Top shots allow fans to collect, share & trade ‘moments’ of their favorite stars (like digital trading cards).

Community via POAPs – Proof of Attendance Protocols enable you to show on your profile attendance to physical events, making it easier to connect with likeminded people.

On-chain ownership: eventually the ownership of your house or your car will be an NFT that you hold in your digital wallet. You will be able to borrow from your house (home equity loan), rent out your car for a weekend (like Turo) or even create an NFT out of the blog post or video you created.

Gaming – the fundamental shift of being able to own the artifacts, loot in the games give players a stake, a reward that was not possible before. Then being able to trade those artifacts for ‘money’ has given rise to the ‘play to earn’ phenomenon – shown eg by Axie Infinity. Granted there is pushback in the gaming community against cheap monetization, so as always the formats will be iterated on.

DAO’s – decentralized autonomous organizations are new ways for communities to organize themselves, and distribute decision making to the community. Quoting from the Bankless DAO article:

“What sets DAOs apart from all previous organizational forms is their flat, decentralized structures and absence of central planning. DAOs share a treasury and raise equity capital through the issuance of their own token, attracting anonymous investors and workers who believe in its mission.

The transparent nature of the blockchain means that all organization’s activities are managed on-chain and anyone can audit its smart contract codes, giving both investors and workers greater transparency into the inner workings of the organization.”

Bankless, Ryan Sean Adams

IMO DAOs are at the earliest stage as they have the promise of re-organizing how we work, how we form communities, how we deliver public goods (see GitCoin), how we do politics (see Andrew Yang on Lobby3).

Move from Proof of Work to Proof of Stake

Ethereum will move to from the current Proof of Work consensus mechanism to “Proof of Stake” within the next 3 months in a process called the ‘Merge”. This will bring the following benefits:

Energy consumption to secure the chain will drop around 99.8%. Instead the chain is secured by having ‘node validators’ stake their ETH (in a smart contract).

The cost of attacking the network will increase, and enable further de-centralization down the road.

In POS – for every new transaction validators can be called randomly to validate whether a particular transaction is ‘valid’ or ‘fraudulent’. If a malicious actor were to send in fraudulent transactions and your node were to validate the transactions as ‘valid’ – the Eth staked on that node would be ‘burned’ (rendered useless). Instead the nodes which validate transactions correctly are rewarded in ETH – currently on the order of around 5% per annum.

Ethereum Scaling

TLDR on scaling: Combined the POS / Layer 2 and Sharding solutions could take Ethereum from the current 15 tps (transactions per second) to 100k tps.

Scaling Ethereum will happen mainly via so called ‘zero knowledge’ roll-ups, or Layer 2 solutions. There are multiple Layer 2 solutions that are built today – but not yet in wide-spread use which enable faster, cheaper transactions.

ZK-roll-ups – such as ZkSync or Starkware enable batching of transactions so that the cost /speed of execution can be reduced by 100x or so. The key is that the code is ‘EVM / Ethereum Virtual Machine’ compatible so it can be deployed very quickly / instantly by a ‘dapp’. If the Dapp has been developed for Ethereum, it would in many cases work ‘out of the box’ with the Zk roll-up as well.

Optimistic Roll-ups such as Arbitrum, Optimism, Metis – bundle transactions as well, and reduce transaction fees by about 50x-100x as well. They have been in use for about one year, but are still experimental. The optimistic roll-ups “optimistically” assume that all transactions are valid during processing, but only validate each transaction later on. This means that it takes up to 7 days to move your funds off an Optimistic Roll-up.

On-chain scaling of the Ethereum main-net will happen via a process called Sharding, which splits the main-net into 64 different ‘shards’ to spread the load. This will happen sometime after the “Merge” – I’m not going to venture a date here… :-).

Ethereum valuation

With staking earning ETH holders ‘dividends’ – Ethereum can be evaluated using business valuation methods. Taking into consideration Ethereum’s growth rate in the past few years and the growing network revenue that will accrue to ETH holders – analysts have estimated ETH to be valued:

Ark invest predicts the Ethereum network could be valued above $20 Trillion in 10 years or 166k / coin

And yes there are risks to these investment theses – competitors such as Solana, Polkadot, Terra, there are geopolitical issues, technical unknowns, malicious actors etc so DYOR. (***This is not investment advice***)

The recap

IMO Ethereum is setup for multiple events that I do not think ‘the market’ has fully priced in, such as:

The coming POS upgrade will enable large institutions to invest as the Proof of Work / ESG complication is removed.

The supply of ETH will drop in June from 12,000 ETH per year to 1,200 ETH per year which will all go to the holders of ETH.

Staking rewards will rise from the current 5% pa to 10-15% pa

ETH is growing like a rocket, with usage up 10x just in 2021

In the aftermath of Canadian truckers and Russian sanctions, the importance of de-centralization will increase, working against ETH challengers like SOL, FTM, Terra etc.

As I argued in my previous post the financial system is broken, and it shows itself for example as the poor are getting poorer and the rich getting richer (US gini co-efficient 1990 – 2020). At the root of the financial system is the US dollar, which is no longer backed by anything else than ‘the might of the US army / IRS’, every dollar is an IOU to some-one else.

The message we hear in main-stream media is that spending is driving the economy, that the ‘mighty US consumer’ keeps the economy rocking and that ‘2% inflation’ is something the Fed should target as a worthwhile goal so that the economy can ‘grow’. Hold those thoughts in your head for a moment.

Does that work on an individual level? If one person spends all their money, and doesn’t focus on their earning power or saving anything – will that work? No, you will go bankrupt.

Does that work on a household level? No of course not – that family would end up on the street sooner or later.

Does that work for a company? A company spending tons on fancy offices, employee salaries, growing like a weed. Sounds like WeWork, and we know how well that worked. It ONLY worked as long as the company was growing.

So WHY in the world do we think that that advice, those policies are good for a nation?

The current consumerist, wasteful, opaque, spend it now messaging is due to the demands of constant growth, which is inherent in a debt-based, inflationary system.

We saw a small deleveraging happen in after the Financial crisis and the whole system almost came crashing down – because otherwise the costs of servicing debt will become un-tolerable.

I predict that the inflationary, fractional reserve, constant growth mandate will sooner or later inevitably meet the limits of a finite, resource constrained world. We are seeing overconsumption of natural resources, overconsumption of calories / energy, leading to climate change and chronic indebtedness – both public and private. There is only so much debt that households and countries can take on – this is shown even by mainstream economists like Rogoff and Reinhart.

The alternative is a deflationary currency that incentivizes actors to save for the long-term – to adopt a ‘lower time preference’. A lower time preference encourages actors to plan long-term, postpone immediate gratification and encourages global collaboration.

A deflationary currency that is immutable – such as gold or Bitcoin, have inherent properties that are favorable for bringing about a lower time preference. The Gold standard worked well for a long time, and IMO a Bitcoin Standard would work fine as well.

Imagine a nation where politicians were not able to spend money willy-nilly, and budgets actually had to be balanced? Increases in bureaucracies would actually be questioned, instead of just pawned off on consumers to pay – eg 95% of new hires in health-care since 1990 have not been doctors, but administrators.

Imagine a nation where wars actually had to be paid for, and you would have to raise taxes if you wanted to go to war? Eg in World War I – the first thing the combatants did was drop the Gold standard. We’ve just seen how we can spend Two Trillion $ in Afghanistan, without real oversight or deliberation. How many less wars do you think we would have had, and could be avoided in the future?

Imagine a financial system where savers, wage-earners, pensioners were able to keep their earnings, savings in the base layer money and actually earn yield on that, instead of being pushed into equities and junk bonds in a reckless chase for yield, chase to keep the value of your ‘monetary energy’ intact.

And finally as as an investor which asset would you prefer to build your financial house on? The Fed balance sheet has almost 10x since 2007, and the USD is getting devalued at the rate of $120 Billion per month. Meanwhile Bitcoin is algorithmically set to get scarcer (new BTC rate is halving every four years), and has a cap of of 21M coins by 2140.

I will argue here that the financial system is broken mainly due to these points:

Currently the rich are getting richer (gini coefficient rising), and the poor getting poorer.

The developed country governments and central banks are having to take on more debt to keep the economy going.

It seems the fractional reserve, debt laden Developed economies are getting more fragile, and more challenged to provide the products and services they have promised to their citizens.

So how did we get here? To understand that we have to go back to 1971, and recap a few things.

Today all money is ‘debt’ – it is a claim on the productive resources in the future. New money is today created in two ways:

The Federal Reserve ‘purchases’ eligible collateral – eg Treasuries, and enters a Debit in their Fed ledger, and Credits one of the ‘money center banks (JP Morgan Chase, Citibank etc)

A bank issues a loan for say a mortgage – the ‘money’ is created into existence by crediting the sellers account with the dollars, the mortgage is created as an asset on the banks balance sheet. The mortgage is the home-owners liability – and when the home-owner pays down the principal, dollars (‘money’) as actually leaving the system.

Due the Vietnam war costing the US too much, and foreign governments pulling their gold from the US, the Nixon administration decided to suspend ‘temporarily’ the convertibility of the US Dollar to gold. The untethering of currency from a gold backing since 1971 has enabled the greatest global monetary inflation ever seen – check out the great site called ‘https://wtfhappenedin1971.com/.

The US economy has grown from 1.2 Trillion USD per year in GDP in 1971 (Revenue) to 22 Trillion USD in GDP in 2020 – about 18x. The average household income was $10,600 per annum, rising to $66,000 per annum – about 6x.

Source: wtfhappenedin1971.com

So while our economy has grown 18x (nominally) and incomes have grown 6x (nominally), let’s look at what happened on the financial side of the ledger.

In 1971 the amount of financial instruments was about 4.5 Trillion in the US – with the bottom of ‘Exters pyramid’ held down by gold:

1971 Money and assets

While Money & assets (not counting derivatives) are over 150 Trillion today – which is a 33x increase.

2020 Money & assets

So to re-cap -incomes have grown 6x, but assets have grown 33x. In my mind these increases in Debt are driving making the rich richer, and the poor poorer:

Source: wtfhappenedin1971.com

To note here – I’m not against rich people per se, most rich people in the US have worked hard most of their lives and I’m sure have earned it. The issue as I see is that the system primarily benefits the ‘Cantillonaires’ today – the megabanks and the 0.1% wealthiest with the first access to money. So while new debt is created – it is mostly an asset for the 0.1%, while it acts as a drag on the economy, for the majority of wage earners.

So who are these Cantillonaires you ask? It’s named after a French economist – Richard Cantillon – who realized that when new money is created – it benefits most those who first gain access to it – they get to enjoy the purchasing power undiluted. By the time that the new money reaches the regular wage-earner, prices and interest rates have risen to account for the new money, so the nominal amount they benefit – say from a stimulus check – is counteracted by the rise in prices.

We also saw in the aftermath of the 2008 financial crisis how we don’t really have a functioning capitalism anymore where those who take risks are allowed to fail (hence ‘too big to fail’). We have instead a capitalism for the cantillionaires, a crony capitalism where the 0.1% reap the profits, but the losses are socialized – i.e. paid for by the tax payers.

Finally today in we are not only taking on new debt, but we are printing more money – the Fed’s is buying 120B in assets (80B in Treasuries, 40B in MBS) – as this extra ‘support’ is needed to carry 30-40% of the US government spending, while it in actuality it is digging a deeper hole for the majority of people. We are following in the footsteps of Japan, down a Keynesian folly where any mishaps are resolved by ‘printing more, stimulating more’. I’d be very interested to discuss or hear how the developed countries are going to get out of this mess we are in today.

Different people in different locations and times have used different instruments – seashells, squirrel hides, large stones and metals to conduct trade. The first commodity money – coins – were minted in Mesopotamia about 5000 years ago.

The key thing here is that money is a human agreement – based on a narrative that recognizes its value. The narrative exists only in a network, and the larger the network the stronger the narrative.

Over time precious metals (mainly gold and silver) emerged as the best monetary instruments – freely chosen by the market because people agreed so, because the monetary metals had these main criteria:

Recognizable

Divisible

Durable

Incorruptible

Scarce

Fungible

Units of account

The First point to understand about ‘money’ is that its value primarily exists due to its salability – to transfer Value over Time and Space.

In a free-market humans have over time selected gold and silver to be used as money, mainly due to the aforementioned criteria – and because you can’t easily find/create more of it compared to existing stock (ie Gold has a High ‘stock to flow’ ratio).

The Second point to understand about Money is that Money is a Network. The more nodes in the network, the more valuable the network becomes – this is often called ‘Metcalfe’s Law’. Only with money in a network can it be used as ‘currency’ or a medium of exchange.

With these two main points established:

Currency / money is a network between humans

Desirable qualities of money resemble those of gold.

..We can then contemplate how should we act should a better money emerge? In a rational, free market humans would choose the money which best fulfills the criteria of money (ie that Best transfer Value over Time and Space).

The case that Bitcoin is better than Gold at being the ‘base layer’ of money is elegantly argued by the Winklewoss Twins in their piece “The case for 500k Bitcoin“.

For example this table shows that in many aspects of being money – Bitcoin is better than gold:

Features of Bitcoin vs Gold

So why do we need a new money or alternatives to the fiat moneys – USDs, Euros and pesetas of the world? Because money is at the base of the financial system, and the current financial system is broken.

The rich are getting richer, the poor are getting left behind -and I will argue in the next post – that no amount ‘UBI’, ‘MMT” or ‘taxing the rich’ will resolve the fundamental issues.

Currencies are in constant competition between each other, and people choose to hold currencies for various reasons. In countries like Argentina, Venezuela and El Salvador people have long held US Dollars, as the US dollar has been a ‘harder’ currency than their own currencies.

So what does it mean that one currency is harder than the other? Easy money will be more easily inflated out of existence, it will not hold its value over time, and conversely the harder money/currency will hold its value better over time.

Before 1971 the world was on a Gold standard, mainly because gold historically has the highest stock to flow at about 71 /1, while silvers’ stock to flow can ramp up to 20/1 .

So how is this relevant to our situation today in 2021?

Saifedean tells eloquently the story of how India and China in the 1800s chose silver as their monetary standard, while Western nations chose gold. Over several decades the corroding effects of constantly slipping purchasing power in China/India meant that the big Asian nations languished.

Compared to the Western countries where the nations/companies/people were able to maintain and even increase their purchasing power, over time meant that the Western nations were able to dominate the world economical, political and military arenas.

To quote from the Bitcoin Standard by Saifedean Ammous:

The demonetization of silver had a significantly negative effect on the nations that were using it as a monetary standard at the time. India witnessed a continuous devaluation of its rupee compared to gold‐based European countries, which led the British colonial government to increase taxes to finance its operation, leading to growing unrest and resentment of British colonialism. By the time India shifted the backing of its rupee to the gold‐backed pound sterling in 1898, the silver backing its rupee had lost 56% of its value in the 27 years since the end of the Franco‐Prussian War.

For China, which stayed on the silver standard until 1935, its silver (in various names and forms) lost 78% of its value over the period. It is the author’s opinion that the history of China and India, and their failure to catch up to the West during the twentieth century, is inextricably linked to this massive destruction of wealth and capital brought about by the demonetization of the monetary metal these countries utilized. The demonetization of silver in effect left the Chinese and Indians in a situation similar to west Africans holding aggri beads as Europeans arrived: domestic hard money was easy money for foreigners, and was being driven out by foreign hard money, which allowed foreigners to control and own increasing quantities of the capital and resources of China and India during the period. This is a historical lesson of immense significance, and should be kept in mind by anyone who thinks his refusal of Bitcoin means he doesn’t have to deal with it.

Ammous, Saifedean. The Bitcoin Standard (pp. 49-50). Wiley. Kindle Edition.

So how does this relate to current events and Bitcoin? I believe the following:

Storing wealth (= saved labor) in a superior currency (Bitcoin) can have long-lasting positive effects, with increasing returns as more individuals, companies and ultimately nations converge on it. This means returns in excess of investment returns to be found in traditional markets.

Why is that? Because Bitcoin introduces a stable system that people can trust, that can not be manipulated or inflated away by any actors, and Bitcoin is programmed to have a high stock to flow ratio. In 2025 Bitcoin will have a higher stock to flow ratio than gold, and the flow is programmed to be halved every four years after that.

Why is this good? Bc as more people learn about Bitcoin, learn WHY they can trust Bitcoin as the hardest, best money in existence, they will want to keep their money (savings) in Bitcoin.Currently only about 5% of people in the industrialized nations have tried cryptocurrency, so the penetration level among individuals is low, and it is almost non-existent among companies and countries.

Why is the current state bad? Because storing wealth in a currency that is depreciating, being inflated away at about 15%-20% per year due to money printing, will have long-lasting deleterious effects in inflating away the stored value that we/you have worked hard to accumulate.

In particular for El Salvador- Bitcoin and the Lightning network allows El Salvadoreans massive efficiency gains by removing the money transfer middle-men that deduct about 4-5% of their GDP.

On Sep 7th 2021 El Salvador became the first country in the world to adopt Bitcoin as Legal tender, and I believe / hope that El Salvador will blaze a path for many other countries to come.

The book “the Bitcoin Standard” by Saifedean Ammous was really influential in convincing me there is value in Bitcoin. Money is a complex, emotionally laden topic, with a rich history, and this book definitively deserves a read. Here is a summary of the 10 key points from my perspective.

#1 Money is a concept

Any value in a currency is an agreement between humans that there actually IS value there. I.e. no chimpanzee will agree there is value in the USD, Yuan, gold, seashells etc. Money – starting out as a medium of exchange – is a concept, such as the nation state or a company and does not ‘exist’ in the physical world.

#2 – Money Transfers Value over Time and Space

For ‘money’ the value primarily exists due to its salability – to transfer Value over Time and Space. In a free market humans have over time selected gold over millennia to be used as money, mainly due to criteria – such as being scarce, it’s divisible, it’s recognizable, other humans agree there is value there and you can’t easily find/create more of it – i.e. it has a high ‘stock to flow’ ratio. (stock to flow ratio means how much exists ‘in stock’ – eg above ground gold – compared to how much new flow – eg gold can be dug up – annually). The high stock to flow ratio is key as it means that the money can’t be inflated by market actors.

#3 – Money is a Network

Currency / money is a network between humans, and desirable qualities of money resemble those of gold. However should a better money emerge (say Bitcoin), in a free market humans would choose the money which best fulfills the criteria of money (ie that Best transfer Value over Time and Space). We have learned the hard way in some countries like Venezuela, Argentina what happens if Money doesn’t transfer Value over time.

#4 Bitcoin is open source Money

The number of Bitcoin is set algorithmically –there will be 21M bitcoins by 2140, the stock to flow ratio of Bitcoin will in 2025 be lower than that of gold, and the flow will be halved every four years.

It is also a remarkable innovation in terms of solving in code the ‘Byzantine Generals Problem’, that is how to co-ordinate distributed forces (think nodes) where some nodes might be traitors or corrupt. This solution establishes a consensus in the network about which transactions are legitimate, so it resolves the double-spending problem.

That is “Bitcoin can be best understood as distributed software that allows for transfer of value using a currency protected from unexpected inflation without relying on third parties”.

#5 Bitcoin network value

You can track the number of humans who agree there is Value in Bitcoin by tracking different metrics – eg market cap, number of wallets, hash rate, price etc. As more people consider it a store of value, that is the price grows higher, it also incentivizes more miners to secure the network – which in turn makes the network safer.

The value in Bitcoin is there due to network effects, and there are real switching costs involved- eg a fork won’t do any good. It’s the difference between an open source library that is copied, waiting to be executed, and a Live network that is running with transactions, users, data etc.

#6 Money printer go “Brrr”

Recent actions by central banks to print money – eg 5 Trillion in the US in response to the Covid pandemic – alter the perception humans have of their national currencies, and as central banks are inflating the supply, they are increasing the flow compared to the stock, and eroding the value in the currency.

While most of the world trusts markets for the pricing, allocation of capital goods – nonetheless there is a central planning board in every country of the world for the most important market – the market of capital.

#7 – Keynesian economics

JM Keynes was an influential economist in the 1930s who has influenced governments around the world that in a recession, governments should ‘stimulate’ the economy to make up for the slack from the private sector. Keynesian economics are the mainstream economics that are taught in Economics schools, opposed to classical/Austrian economics, with one of the main tenets of Keynesianism being that inflation is good, and should be ‘managed’ to about 2% per year. What is then not often mentioned is that the money in your wallet declines by 2% per year.

Ammous points out the example of the ‘depression that never happened’ – in 1921, where the government did not take ANY action, wages initially dropped 10%, but within 9 months the economy was strongly growing again leading to the ‘roaring 1920s’.

This is in opposition to the Depression in 1933 where the government froze wages, stimulated with public works programs and by confiscating US gold reserves, and eventually devalued the dollar 70% from $20/oz of gold to $35/oz.

#8 – A deflationary currency leads to lower time-preferences

An individual with a low time preference chooses to defer gratification, and work on items where the pay-off is further out in the future. We know from psychology this is good for individuals, and economics tells as investment in the future is beneficial. Therefore a money that is deflationary, that retains or increases in value, should be preferred by society and individuals alike.

However the opposite is taught today as beneficial – more consumer spending to satisfy cravings, wants, and less saving is good. Less capital therefore available for investment and growth, and pressure on companies to perform in the short term.

#9 – Bitcoin as a concept is many things

A concept has the ability to be multiple things at the same time – that is Bitcoin was initially planned to be a digital currency to be used for day to day purchases, however at the moment due to the price volatility and transaction speeds it is not feasible for that at the moment. There are eg second layer solutions (eg Lightning network or Strike ) that are working to resolve the issues. Taxation issues would have to be resolved as well.

#10 – Bitcoin as an option / hedge

Currently Bitcoin can more appropriately be thought of as

an option (hedge) towards central banks eroding the value in national currencies

an option on a true global money

a volatile investment with a lot of possible upside

but also a chance of going to zero.

If you’ve made it this far – I will again recommend you check out this book – “the Bitcoin Standard” by Saifedean Ammous. It can change how you think about money, as it did for me.

I’ve been thinking about what money is , what it will be in the future for a while now. I own some minimal stakes in BTC, ETH – for now to be ‘along for the ride’ and partially as a hedge against central banker mistakes. Central bankers may have PhDs, but we’re all human, and I don’t think they know the future. (Before we jump in -if you need a primer on cryptocurrencies, you can for example read Mark Susters’ great piece on cryptocurrencies – the cases for and against.)

Writing this in August 2020, we are in the throes of the COVID-19 pandemic, and the US Federal Reserve has just deemed it necessary to expand their balance sheet by about 5 Trillion USD.

My main premise in this post is that every-one should seriously learn about cryptocurrency today, and potentially invest a small stake to better understand the ‘nature of this particular beast’. It could be very important.

So why now?

The 5 Trillion in new money from the Federal Reserve will flow out into the economy via the commercial banks, from there to the larger companies, regional banks and from there on down to Main Street. Unfortunately the current financial system is leading to greater concentrations of wealth – the 0.1% getting richer and richer, while the 80% struggle with the cost of basic goods (food, health care, education, housing etc) increasing. We can already see it in that the stock market as of now is back to all-time highs, while on Main street the unemployment rate is high and many small businesses are turning off the lights.

Most people don’t think about the role of our country’s currency – and one of the key points which argue against cryptos becoming mainstream is the level of ignorance most people have re: what money/ currency – really is.

So understanding the different characteristics of money is a good starting point:

store of value – it needs to keep it’s value, be relatively stable

medium of exchange – you need to be able to transact with it

fungibility – one ‘dollar bill’ needs to be exactly the same as the next ‘dollar bill’

recognizability – you need to know it when you see it

unit of account – you need to be able to split it and record it in myriad ways

Fiat money vs commodity money – and finally – it will be either ‘fiat’ – that is credit money, or it will have some backing to it (like gold).

How many people you associate with understand these characteristics, and have questioned these for your country’s currency? In most developed countries most people just ‘use’ money, like clean water coming from the taps. We don’t have to understand how it got there.

We don’t use the Dollars, the Euro’s because they are excellent mediums of exchange or stores of value. I’ve lived in three developed countries (Finland, Singapore, US) and I can tell personally it didn’t really matter whether I was transacting in SGD, EUR or USD. The features were the same, you’d earn very little interest and lose out on inflation if you held cash in those. Today’s money is primarily a ‘unit of account’ that you use to track your income, spending, loans and savings – and for most people they don’t question WHAT that base unit actually IS.

Another main reason we use currencies today is because the government in the country where we reside are legally requiring (‘forcing’ to use the libertarian lingo) us to use that currency – at least for paying taxes. I fully agree that governments will NOT cede monetary control easily – since the whole government & country apparatus is transacting in that particular currency, and the government benefits from what’s called ‘Seigniorage‘ – that is where sovereign-issued securities are exchanged for newly-printed banknotes by a central bank, allowing the sovereign to “borrow” without needing to repay.

Understanding that modern money is based on the electronic deposit system controlled by the banking system, and that this Fiat money is created as credit through the loan creation process, is crucial. In today’s electronic money system money exists largely as a record of account in databases as a result of the money being created via loan generation. Meaning that all of the ‘money’ in today’s world are actually just IOU’s. This also means that the USD’s , EURs of the world need to have inflation, as you and I need oxygen. We saw in 2009 what happened when even small amounts of deflation threatened to bring down the whole deck of cards.

So why is a deflationary currency better? Glad you asked.

Because with a deflationary currency (eg Bitcoin) it would not be possible to ‘bail out’ Wall Street / speculators who have used too much money on stock buy-backs over the last 10 years, and kept nothing in reserves. We are rewarding stupidity – the bankruptcy process is needed to dis-incentivize speculation.

An inflationary currency allows us to inflate and borrow almost limitless amounts, and spend money we don’t have – sacrificing not only our own futures, but our children’s future. A deflationary currency focuses you to spend on what you truly need, and some wants. It’s better for the environment, because you will not buy unnecessary ‘stuff’ because your money will be worth more in the future.

A gold-backed currency is inherently deflationary – the US Dollar was gold-backed until 1971, and folks back then didn’t die of a ‘deflationary death spiral’ as some would want you to believe. Some of the greatest ‘real’ – (i.e. growth in earnings / wealth, accounting for inflation) – growth periods in US history happened in the 1870s-1880s with rail-roads being built, industrialization getting started.

With eg Bitcoin there is a fixed limit to the number of Bitcoin that will ever be released, and the mining process is ardous and expensive, so there is a mathematical guarantee that only a certain number of Bitcoin will ever be created (21 million to be exact, by 2140). The Bitcoin Blockchain has not been hacked since it’s inception in 2009, and I would suppose the likely hood is extremely low.

So how could a transition to using more Crypto / Bitcoin then happen? One route is via the recognition of wider parts of the population – eg because of a currency crisis – that a crypto can provide a better store of value – eg ‘Bitcoin as digital gold‘. Currently it’s more of an option / hedge as mentioned.

Also if there is a wider recognition, adoption, then it should naturally lead to Gresham’s law (bad money drives good money out of circulation) – people holding that currency (eg crypto) for it’s value preservation abilities, and transacting in some other medium of exchange. Basically if you’ve bought Bitcoin, you would hold them as you’d believe they will store value / appreciate in the future – and you would transact in your local fiat currency.

Eventually you would also want to start getting paid in crypto (more value) instead of the fiat, should the ball start rolling this way.

To sum it up – I don’t have a crystal ball, and can’t predict the future – and have yet to find any-one that can. So pls consider these points:

The current monetary system seems to reward a very small portion of humanity disproportionately – why not try to find a better tool in this arena?

As humans we are experimenting with different technologies and tools all the time, so shouldn’t we try to discuss, experiment and improve also on how money works, rather than leaving it to a select committee?

Given what we know about human fallibility and central banker prediction capabilities – is it not prudent to have a small portion of ones net-worth invested in alternative vehicles (like crypto, gold) that are not tied to the current monetary systems?